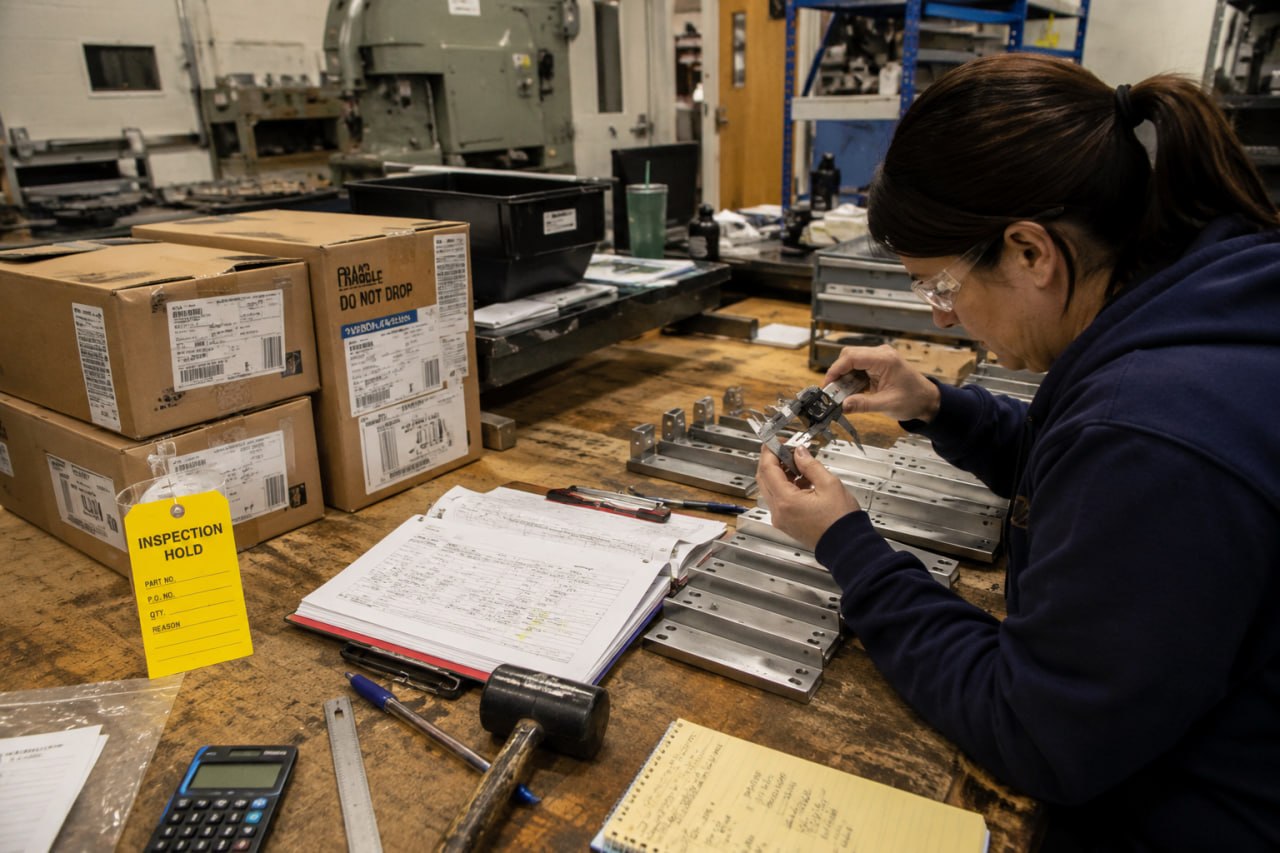

Quality Costs Are Becoming a Supplier-Risk Problem

Quality is usually treated as a shop-floor discipline: inspection plans, first articles, nonconformance reports, rework loops, and the long argument over whether a defect came from design, process, material, or operator error. The current supplier environment is making that view too narrow. Quality now has to be managed as a supply-chain risk, because the part arriving at the dock may have changed before it ever reaches the line.

What makes this worth attention now is that quality risk is moving upstream at the exact moment sourcing decisions are getting more volatile. Tariffs, component shortages, supplier substitutions, and cost pressure are no longer just purchasing problems. They can change what shows up at the dock and quietly push hidden costs into inspection, rework, scrap, and delayed production.

That is the useful signal in Lumafield’s new Cost of Quality report, released May 19 with survey work from NewtonX. The headline number is blunt: 62% of surveyed manufacturing quality leaders in the U.S. and Canada said tariffs and other trade barriers have made it harder to ensure product quality. Supplier-related quality issues were the top concern across the represented industries, and 41% of respondents said a 25% reduction in supplier-related quality issue costs would have the greatest operational impact.

The report is from a company that sells industrial CT scanning and analysis software, so its commercial point of view should be kept in mind. Even with that caveat, the data maps closely to what many smaller manufacturers already feel: the quality problem is no longer limited to catching bad parts. It is also about detecting supplier drift, substitutions, opaque provenance, late changes, and inspection labor that quietly consumes margin. The report is useful because it turns a technology pitch and a generic reminder that quality matters into a practical warning: if supplier-driven quality costs are not measured clearly, a cheaper quote can easily become the more expensive option.

The most practical finding is not that manufacturers care about quality. They always have. The practical finding is how poorly many companies can see the actual cost. Lumafield says 40% of surveyed organizations estimate quality-related costs at 2-5% of revenue, while 42% put the figure above 5%. More important, 58% believe at least a quarter of their true quality costs go unaccounted for. Only 35% of surveyed decision-makers use a comprehensive cost-of-quality model.

For a small shop, that measurement gap matters more than the exact survey percentages. If rework is logged only as a late traveler note, if inspection time is buried inside general labor, if supplier defects are handled through phone calls instead of structured claims, the business cannot tell whether a new vendor is actually cheaper. The purchase price may fall while receiving inspection, sorting, scrap, expedited replacement orders, and customer containment eat the savings.

Trade volatility makes that worse. The survey says 71% of respondents cited component shortages as the largest impact from tariffs and trade barriers. More than half said suppliers have downgraded product quality to offset tariff costs. More than a quarter said overseas suppliers have concealed the real country of origin of products to evade tariffs. Those are serious claims, and any individual buyer should verify them rather than treating a survey as proof against a specific supplier. But they point to a real operating pattern: when cost pressure hits the supply base, quality risk often shows up as material substitutions, looser process control, alternate sub-tier suppliers, and paperwork that arrives cleaner than the parts.

This is where smaller manufacturers need a different playbook. The first step is not buying the most advanced inspection system. The first step is making supplier quality visible enough to manage. Track defects by supplier, part family, defect type, lot, corrective action, and cost bucket. Separate internal process scrap from incoming supplier issues. Put inspection labor into the cost model instead of treating it as unavoidable overhead. When a supplier change coincides with longer receiving queues or more engineering review, count that time.

That also means treating sourcing as a test-first process. Before a shop trusts a new supplier, cheaper material, changed route, or replacement component, it needs a simple way to verify what changed and what that change costs. The business needs to know whether the part passed inspection and what it had to spend to prove the part was usable.

The second step is to tighten the receiving plan around risk, not habit. Stable commodity parts do not need the same scrutiny as a newly sourced casting, a safety-critical machined component, a polymer part with material sensitivity, or an electronics assembly coming through a changed trade route. Shops can use tiered checks: documentation review for low-risk items, dimensional sampling for moderate-risk lots, and deeper inspection or outside lab work when the failure mode justifies it. The goal is not inspection for its own sake. The goal is fast, defensible escalation when a supplier starts drifting.

That creates an operator and training issue too. Receiving teams, inspectors, and floor leads need clear defect categories, escalation rules, and a consistent way to log supplier drift. If inspection, rework, sorting, and engineering review are buried inside normal labor, the real cost stays invisible, and purchasing decisions keep being made from incomplete numbers.

The third step is to connect quality data to purchasing decisions. Supplier scorecards often overemphasize on-time delivery and quoted price because those numbers are easy to find. Cost of quality turns the conversation toward total burden: how many incoming lots required sorting, how often engineering had to approve deviations, how much production time was lost waiting on replacement material, and how often customer due dates were protected by overtime. A supplier with a higher unit price may be the lower-cost option if it keeps the line predictable.

Automation has a role, but the caveat is important. Lumafield notes that 77% of surveyed organizations still rely on manual visual inspection, and nearly half spend 5-10% of production labor hours on inspection. That creates an opening for machine vision, CT, automated gauging, and AI-assisted review. It does not mean automation should be dropped into a vague quality process and expected to fix it. Automated inspection is most useful when the shop already knows the critical characteristics, the defect modes, the sampling strategy, and the decision rule for what happens when the system flags a part.

For job shops and small manufacturers, the takeaway is to put supplier quality into the quoting and sourcing system instead of leaving it with the inspection department. Ask what a new supplier will cost to qualify. Ask which incoming characteristics are tied to customer risk. Ask how quickly a defect can be traced back to a lot and purchase order. Ask whether the current ERP, QMS, spreadsheets, or paper travelers can show the real cost of supplier variation without a week of manual reconstruction.

Quality discipline has always protected customers. In the current supply environment, it also protects margin. Quality is becoming a sourcing risk as well as an inspection function. The shops that can see the full cost of supplier variation — inspection labor, sorting, rework, scrap, delays, and customer containment — will make better purchasing decisions than shops comparing unit price alone. The next signal to watch is whether manufacturers start building supplier cost-of-quality data into scorecards, quoting, and vendor qualification instead of treating it as a back-end quality problem.